ATO Tax Crackdown – What You Need to Know Before You Lodge Your Next Tax Return

Understand what you can and can’t claim in your next tax return

The Australian Taxation Office is...

Making personal contributions to super is one way you can minimise your tax bill and may leave you with more cash in the bank in the long run. When you’ve got a fair bit of cash saved up or receive a significant lump sum of money, the common advice would be to use that money to pay off big debts such as a home loan. But there is another way to use that income that may give you a bigger saving. Continue reading to find out why.

The example below is general in nature and does not constitute financial advice as it does not take into consideration your personal circumstances. If you’d like more information or advice, please get in touch with the YOUtax.

A Concessional Super Contribution is a contribution made to a super fund with pre-taxed funds. For example, your Employer Super Contributions (SGC) or any super contributions you make through salary sacrifice. These funds are charged a concessional tax rate (currently 15%) which is usually lower than the tax paid on your normal salary/income.

If you make a voluntary contribution to your super after you’ve already paid income tax on it, this can be reclassified from non-concessional (tax paid) to concessional (pre-tax) by claiming a 100% tax deduction in your Income Tax Return. You will need to complete a Notice of intent to claim and send to your super fund.

If your income + superannuation contributions are above $250,000 per year your concessional superannuation rate is subject to Division 293 Tax, which is an additional 15% on top of the concessional rate (i.e. it is taxed at 30%). That additional 15% is levied on the excess above $250,000 or the total superannuation contribution – whichever is the lesser.

As of 1 July 2021, you and your employer can contribute up to $27,500 combined into your super fund and it will be taxed (directly from your super fund) at the concessional rate of 15%. This maximum amount ($27,500) is known as a “concessional contributions cap”.

If you exceed your annual cap, you will be charged an excess concessional contributions charge (ECC Charge) calculated by the ATO, and your excess contributions will be taxed at your marginal tax rate through an automatic amendment from the ATO.

If you don’t reach or exceed the concessional contributions cap, any remaining amount under the cap is “carried over” into the following year. That means if you earn more in the following year, you can make a bigger contribution to your super and still be taxed at 15%.

Concessional Contributions Caps |

Unused Concessional Contributions |

|||

Financial Year |

Annual Cap |

Employer Contributions |

Personal Contributions |

Unused Cap |

|

2023 |

$27,500 |

$12,000 |

$7,800 |

$7,700 |

|

2022 |

$27,500 |

$12,000 |

$7,800 |

$7,700 |

|

2021 |

$25,000 |

$9,500 |

$2,800 |

$12,900 |

|

2020 |

$25,000 |

$8,550 |

$- |

$16,400 |

|

2019 |

$25,000 |

$8,550 |

$- |

$164000 |

| TOTAL CARRIED FORWARD UNUSED CONTRIBUTIONS = $61,100 | ||||

There are a few scenarios where you can "carry over" your super contributions and make the most of the concessional tax rate:

|

Contributing to the First Home Super Saver (FHSS) SchemeYou can use your unused concessional contribution caps and/or carried forward balances toward the First Home Super Saver (FHSS) Scheme and contribute up to $15,000 in personal contributions per year. |

|

When your income increases to over $180,000 - $200,000This pushing you into the highest tax bracket, you may like to take advantage of substantial tax minimisation opportunities before your Division 293 tax rate kicks in at $250,000 and increases your tax on super by an additional 15%. |

|

When your superannuation balance is nearing $500,000If you have unused concessional contributions, it may be your final opportunity to contribute and receive a tax benefit. |

|

If you’ve received a large sum of money as an inheritanceAs the baby boomers age, we are seeing large amounts of wealth move from one generation to the next. You pay tax on any interest earned if those large sums of money sit in your bank account. You can utilise your tax-free inheritance to carry forward your unused caps and make a concessional contribution to super. |

|

Preparing for retirementTaking advantage of unused concessional contributions with higher super contributions can support individuals with no mortgage or little debt and more cash flow. |

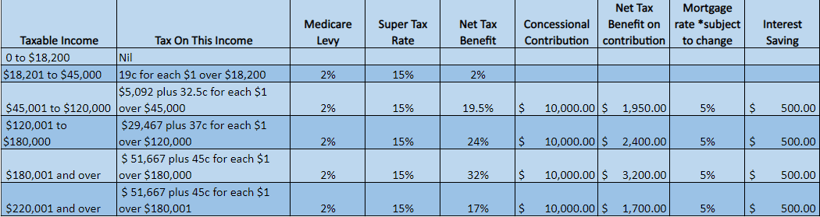

With interest rates on mortgages are currently between 3% - 4% you may like to consider more tax-beneficial opportunities across the various income levels. The table below illustrates how contributing to concessional contributions provides a larger Net Tax Benefit compared to the savings made when offsetting a home loan:

Carl is earning $200,000 a year and has $35,000 in unused or “carry over” concessional contributions. His super balance is under $500,000.

Based on the ATO's income tax rate table, Carl's income above $180,000 is taxed at 45%.

Any personal contributions he makes to his super fund will be taxed at 15% (that’s a 30% saving on the tax he has to pay on any money he deposits into his super).

If he contributes $20,000 towards his super, that reduces his taxable income to under $180,000 and puts him in a lower tax bracket of 37%. Instead of owing 45% tax ($9,000), he only owes 15% tax ($3000) that is paid from his super fund, not his personal savings.

Carl can use that difference of $6,000 towards his home loan.

In comparison, if Carl had used that $20,000 to pay off a fixed-rate mortgage, he would only be saving approx 5% estimated interest rate or $1,000 (based on a simple interest calculation).

To find out how much you’ve contributed towards your concessional contributions cap, ask your tax accountant or locate the information in your myGov account.

If you log into your ATO account through myGov, you will find your super balance as at 30 June of the last financial year, and a list of annual contributions made and unused concessional contributions available.

The ATO keeps an automatic record and also reconciles your superannuation caps each year. You do not need to inform them if you go over your annual cap.

YOUtax is an award-winning digital accounting firm on a mission to make tax and financial wellness services easily accessible to everyone who needs it. We partner with organisations to provide time-poor employees across Australia with an easy-to-access and easy-to-understand Financial Wellness Program that includes education, tax planning and advisory services.

Winners of the 2021 Australian Accounting Awards Innovative Firm of the year and awarded Xero’s Innovative Partner of the Year for 2022.